- Home equity loans and HELOCs offer the lowest rates (approximately 7-9% in March 2026) — the best financing path if you have 20% or more equity and a credit score above 680.

- Contractor point-of-sale financing (0% for 12-18 months) is available through GreenSky, Hearth, and Regions Bank with no equity required and approval in minutes.

- FHA Title I loans allow up to $25,000 for roof replacement without requiring home equity, with fixed rates and terms up to 20 years.

- The average financed roof project runs $12,000-$16,000 — monthly payments on a 10-year home equity loan at 7.87% come to roughly $146-$195 per month.

- Delaying a roof replacement is almost always the costlier decision: a $900 leak left unaddressed for 12-18 months routinely becomes $7,000-$12,000 in sheathing rot and structural repair.

A roof replacement is one of the largest single-line expenses a homeowner faces. National averages sit between $9,000 and $18,000 for a standard asphalt shingle replacement [1], and in high-labor markets or on complex rooflines those numbers climb further. Most households cannot absorb that cost from savings alone, and most do not need to. Five well-established financing paths exist in 2026, each suited to a different financial profile.

For full context on what drives replacement cost in the first place, review the complete roofing costs guide before committing to a financing path. Understanding the total project scope first prevents you from under-borrowing and returning to a lender mid-project.

This article walks through each financing option in plain terms: how it works, what it costs today, who it fits, and where it falls short. A comparison table, a real-world case study, and eight frequently asked questions follow.

Get quotes from top-rated pros.

Option 1: Home Equity Loan

A home equity loan is a second mortgage that lets you borrow a fixed lump sum against the equity you have built in your home. The loan carries a fixed interest rate, a fixed monthly payment, and a fixed repayment term — typically 5 to 15 years for a roofing project. Because the loan is secured by your home, lenders price it well below unsecured alternatives.

2026 rates: The national average home equity loan rate sat at 7.87% as of mid-February 2026, with well-qualified borrowers (credit scores above 740 and loan-to-value ratios below 70%) accessing rates as low as 6.50% [2]. Borrowers with scores in the 640-679 range typically see rates of 9-10%.

Requirements: Most lenders require 15-20% remaining equity after the loan closes, a credit score of 640 or higher, verifiable income, and a debt-to-income ratio below 43%. Approval and funding typically take 2-4 weeks.

Loan amounts: $5,000 to $100,000 at most major lenders — the full range of residential roofing projects falls comfortably within this window.

Tax note: Interest on a home equity loan used for a qualifying home improvement may be deductible if you itemize, subject to IRS limitations on total mortgage debt. Consult a tax professional to confirm eligibility for your specific situation.

Monthly payment table — $14,000 project, 10-year term

Monthly payment table — $14,000 project, 10-year term

| Credit Score Range | Typical Rate (2026) | Monthly Payment | Total Interest Paid |

| 740+ | 6.50% | $158 | $4,962 |

| 700-739 | 7.87% | $167 | $6,072 |

| 680-699 | 8.75% | $175 | $6,990 |

| 640-679 | 9.50% | $181 | $7,752 |

Pros: Predictable fixed payment, lower rate than unsecured options, potential tax deduction, loan amounts match roofing projects precisely.

Cons: Home is collateral, closing costs typically add $500-$2,000, and the 2-4 week approval timeline is not suitable for emergency roof situations.

Option 2: HELOC (Home Equity Line of Credit)

A HELOC is a revolving credit line secured by your home equity. Unlike a home equity loan, you draw funds as needed during the draw period (usually 10 years) rather than receiving a lump sum at closing. The rate is variable, tied to the prime rate, which stood at 6.75% in March 2026 [3].

2026 rates: The national average HELOC rate was 7.23-7.31% in late February and early March 2026 [3], placing it slightly below average home equity loan rates at this moment in the rate cycle. Most lenders price HELOCs at prime plus 0.50-2.00%, so borrowers with stronger profiles land closer to the lower end.

Draw and repayment structure: During the 10-year draw period you pay interest only on what you have drawn. After the draw period closes, repayment begins on the outstanding balance over a 20-year period. That transition can create payment shock if a large balance remains.

Best use case: A HELOC makes more sense than a home equity loan when the project scope involves more than roof replacement alone.

If you are doing a roof replacement, gutters, and siding over a 12-18 month window, a HELOC is the right tool. You draw for each phase, pay down between phases, and keep your credit line available. For a single roof job with a firm contractor bid, a home equity loan's fixed payment is cleaner and removes any rate risk.

Cons: Variable rate creates payment uncertainty. If the prime rate rises 1-2 percentage points before you pay off the balance, your monthly obligation increases. Home remains at risk of foreclosure if payments lapse.

Option 3: Contractor Point-of-Sale Financing

Most licensed roofing contractors partner with one or more third-party lenders to offer financing at the point of estimate or contract signing. The most common platforms are GreenSky, Hearth, Regions Bank, and Synchrony Bank. Approval is typically instant or within 2-3 minutes based on a soft credit pull.

Common plan structures:

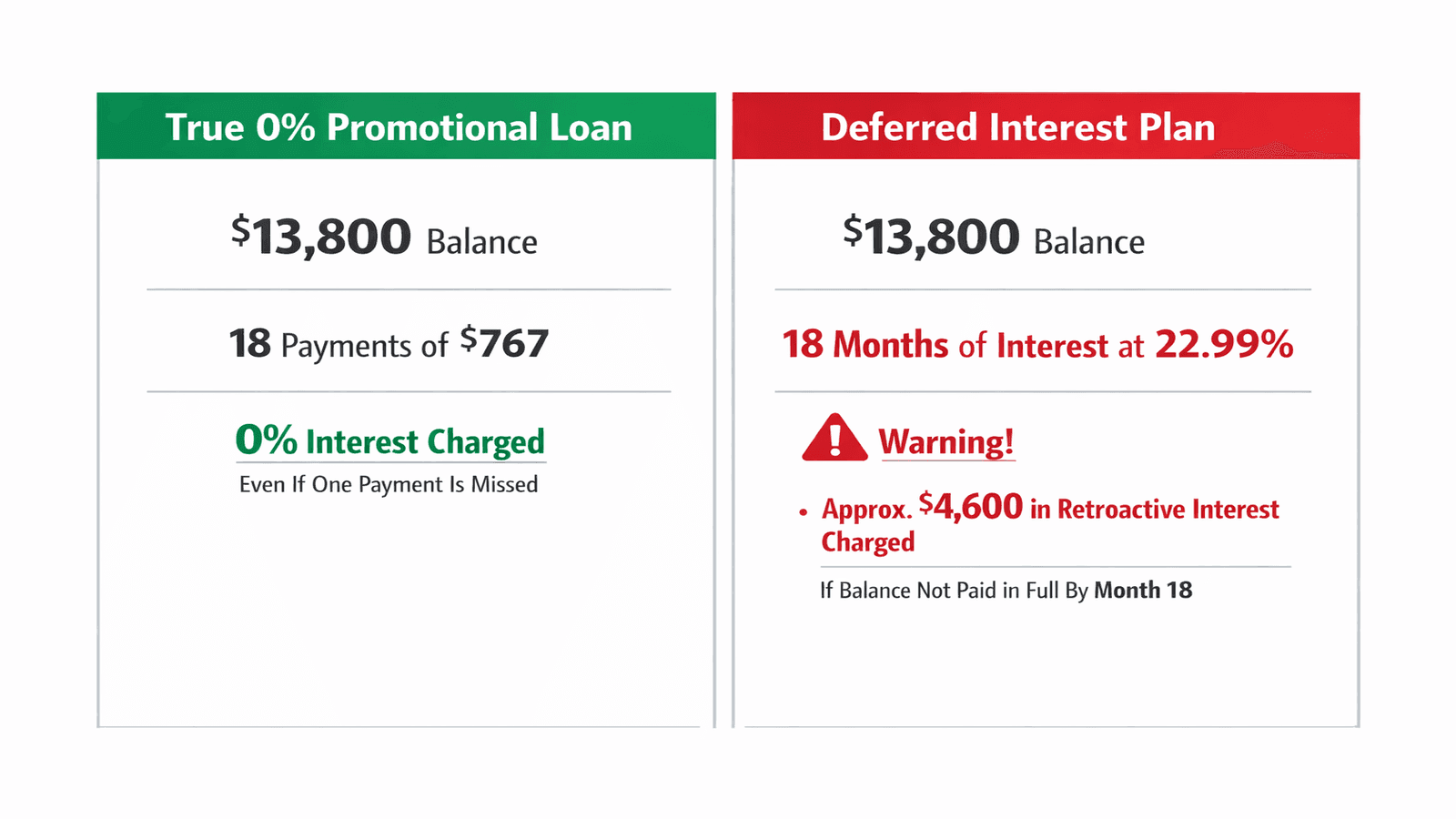

- 12-month true 0% interest: No interest if the full balance is paid within 12 months. If not paid in full, standard rate kicks in for the remaining balance going forward. This is a true promotional rate with no retroactive interest.

- 18-month deferred interest ("no interest if paid in full"): Interest accrues from day one at a rate of 17.99-24.99% but is waived entirely if the full balance is paid before the promotional period ends. If one dollar remains at month 18, all deferred interest — on the original balance — is charged immediately. This is not the same as a 0% loan.

- 60-month fixed installment: Rates typically run 12.99-15.85% APR through GreenSky for this term [4]. Monthly payments on a $14,000 project at 13% over 60 months equal approximately $317.

NearbyHunt network insight: Roofing contractors in the NearbyHunt professional network report that 35% of their customers use contractor financing. Of those, the majority choose a 12-month or 18-month promotional plan and pay the balance off before the deadline, effectively financing the project at zero cost.

Contractor financing comparison table

Get quotes from top-rated pros.

Contractor financing comparison table

| Product | Rate | Term | Min Credit Score | Deferred or True 0%? |

| GreenSky 0% promo | 0% promo / 17.99% standard | 12-18 months | ~600 | True 0% (if paid in full) |

| GreenSky fixed installment | 12.99-15.85% APR | 60-120 months | ~600 | N/A (standard fixed) |

| Hearth marketplace | 8.99-35.99% APR | 24-84 months | 600+ | N/A |

| Synchrony PPRO | 0% promo / 26.99% standard | 6-24 months | 620+ | Deferred interest (read terms carefully) |

Critical distinction: Always ask the contractor whether you are receiving a true 0% promotional loan or a deferred interest plan. They look identical on a monthly statement during the promotional period. They are not identical if you carry a balance past the deadline.

Loan amounts: Most platforms finance between $2,000 and $65,000, covering the full range of residential roofing projects.

Option 4: Personal Loan

A personal loan is an unsecured installment loan that requires no home equity and no collateral. Approval is based entirely on creditworthiness and income. Funding is typically available within 1-3 business days.

2026 rates: Personal loan rates vary far more widely than equity-secured products. LightStream starts at 6.49% APR with AutoPay for borrowers with excellent credit and offers repayment terms up to 20 years for home improvement purposes [5]. SoFi starts at 8.74% APR with autopay and direct deposit enrollment [5]. Borrowers with fair credit (scores in the 600s) may see rates of 18-24% or higher from online lenders.

Amounts: $2,000-$100,000 depending on lender and credit profile.

Best fit: Homeowners with little or no equity, renters who need structural repairs before selling, or emergency situations requiring funding within 48 hours. Also appropriate for homeowners with strong credit (720+) who want to preserve equity for other purposes.

Best sources for personal loans: Credit unions typically offer the lowest rates for members. Online lenders including LightStream, SoFi, and Marcus by Goldman Sachs provide fast decisions and transparent rate shopping without hard credit pulls in the pre-qualification step.

I only recommend personal loans when someone needs the roof done immediately and has no equity access. At 18% interest you are paying $250-$300 per month on a $14,000 loan over five years. That is $6,000 in interest for what is essentially a 5-year loan on a 30-year asset. If you can wait 3-4 weeks and tap equity instead, you will save thousands.

Downsides: Higher rates than any equity-secured option, not tax deductible, and the shorter maximum terms of some lenders (SoFi caps at 7 years vs. LightStream's 20) can result in higher monthly payments on larger projects.

Option 5: FHA Title I Home Improvement Loan

The FHA Title I program is a federally backed loan specifically designed for home improvements on primary residences. It does not require home equity to qualify, making it accessible to homeowners who have purchased recently or are in markets where values have not appreciated enough to generate substantial equity.

Loan amounts: Up to $25,000 for a single-family home, unsecured (no lien required on the property). Loans up to $7,500 are available with only a signature. Loans above $7,500 require a security interest in the property [6].

Rates: Fixed rates set by the individual HUD-approved lender, typically negotiated between lender and borrower. Current market rates for FHA Title I loans fall in the 7.5-9.5% range depending on lender and borrower creditworthiness.

Terms: Up to 20 years for amounts above $7,500.

Requirements: The home must be your primary residence occupied for at least 90 days. There are no minimum credit score requirements set by HUD, though individual lenders set their own thresholds. Income verification is required. The loan must be used for improvements that protect or improve the livability of the home — roof replacement qualifies directly [6].

How to apply: Locate a HUD-approved Title I lender at HUD.gov. There is no requirement to use a specific contractor; you may work with any licensed roofing contractor. Processing time is typically 3-6 weeks.

Best fit: Homeowners with limited equity but established income and credit history, and those who want a federally backed fixed-rate product without putting their home up as collateral beyond the minimal security interest required for larger amounts.

Insurance Reimbursement as a Financing Strategy

For homeowners who experienced a qualifying weather event, homeowners insurance can effectively eliminate most of the out-of-pocket cost of a roof replacement. Hail and wind damage claims routinely result in full replacement coverage after the deductible.

How RCV policies work: Replacement Cost Value (RCV) policies pay in two stages. The insurer releases Actual Cash Value (ACV) upfront — the depreciated value of the old roof. After the work is completed and verified, the insurer releases the remaining depreciation, bringing the total payment to full replacement cost.

Supplementing underpaid claims: If the initial adjuster estimate misses line items or undervalues materials, a licensed contractor can prepare a supplement for additional scope. Most experienced roofing contractors are familiar with the supplement process.

Deductible financing: Some contractors offer to finance the deductible amount. State laws on this vary; some states prohibit contractors from waiving or financing deductibles as it constitutes insurance fraud. Verify your state's regulations before proceeding.

Emergency advance payments: Many insurers offer an advance draw against the claim for emergency tarping and temporary protection. This prevents further interior damage while the claim is processed.

If you had a hail event or high-wind storm in the past 12 months, call your insurance company before you call a roofing contractor. A $13,000 replacement might cost you only your $2,000 deductible if you have the right coverage. Over 1,800 projects in my career, the number of homeowners who paid out of pocket when insurance would have covered the job is a number I hate thinking about.

Get quotes from top-rated pros.

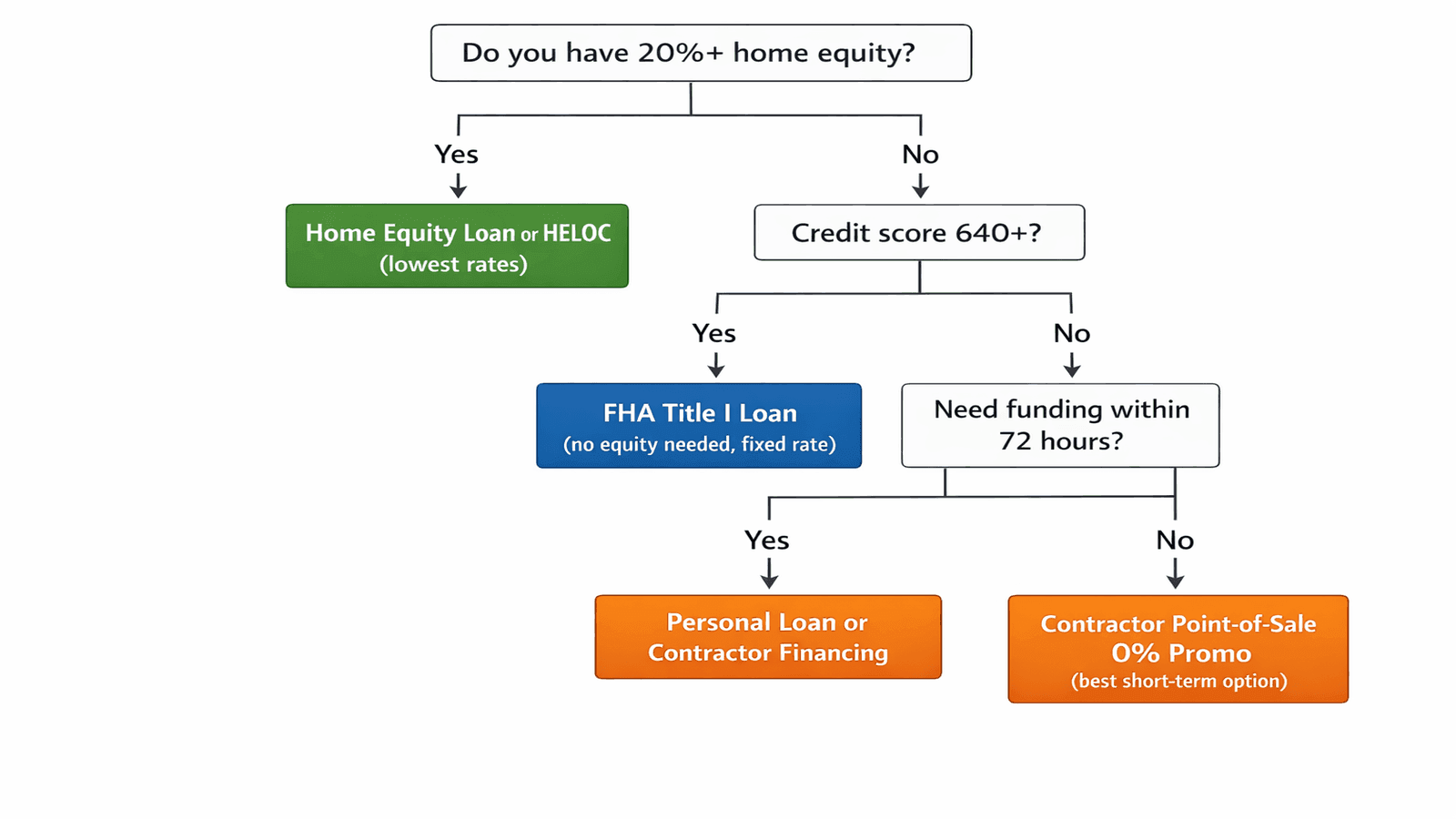

How to Choose the Right Financing Option

The right financing path depends on your equity position, credit score, project urgency, and how much total interest you are willing to pay. The decision framework below covers the most common scenarios.

Decision logic:

- Do you have 20% or more equity and a credit score above 640? Start with a home equity loan for the lowest fixed rate.

- Is your project multi-phase (roof plus other work over 12+ months)? A HELOC preserves flexibility.

- No equity but good credit and no immediate urgency (3-6 weeks available)? FHA Title I provides a federally backed fixed rate without equity requirements.

- Need funding within 48-72 hours? Personal loan or contractor financing.

- Credit score 600-640 with no equity? Contractor point-of-sale financing is the most accessible option.

Monthly payment comparison — $14,000 project

Monthly payment comparison — $14,000 project

| Option | Rate | Term | Monthly Payment | Total Interest Paid |

| Home equity loan | 7.87% | 10 years | $167 | $6,072 |

| HELOC (interest-only draw period) | 7.23% | Draw period | $84 (interest only) | Depends on balance |

| Contractor 0% promo | 0% | 12 months | $1,167 | $0 (if paid in full) |

| Contractor fixed installment | 13.99% | 60 months | $325 | $5,500 |

| Personal loan (good credit) | 10.99% | 60 months | $305 | $4,280 |

| FHA Title I | 8.50% | 10 years | $174 | $6,848 |

Cash or check discount: Paying a contractor in full by check or ACH sometimes yields a 2-5% discount that lowers the effective project cost. This applies when the contractor avoids dealer fees associated with financing platforms. Always ask.

Tax deductibility: Only home equity loans and HELOCs where the funds are traceable to a home improvement may qualify for interest deductibility. Personal loans and contractor financing do not qualify. Confirm with a tax professional.

Real-World Case Study

Emily T., Memphis, Tennessee, received a roof replacement estimate of $13,800 after a hail event was ruled insufficient for an insurance claim (the storm did not meet her insurer's minimum damage threshold). Emily had approximately $6,000 in usable home equity and a credit score of 715 — enough equity for a small home equity loan but well below the project cost.

She evaluated two paths:

Option A — Personal loan at 11.5% over 7 years: Monthly payment of $232. Total interest paid over the life of the loan: approximately $3,660.

Option B — GreenSky 18-month 0% promotional financing (true 0%, not deferred): Monthly payment of $767 to pay off the $13,800 balance in 18 months. Total interest: $0.

Emily chose Option B. She verified with the contractor that the plan was a true 0% promotional loan — not a deferred interest plan — and confirmed the terms in writing before signing. She structured her monthly budget to pay $767 per month and paid off the balance in 16 months, two months ahead of the deadline.

In James Carver's words: "Emily's approach was textbook. She compared the total interest cost across options, asked the right question about deferred versus true 0%, and set the monthly payment high enough to guarantee she finished before the deadline. The 18-month window is generous if you plan to use it."

The lesson: contractor financing at 0% is genuinely the lowest-cost option when the promotional period is long enough and the borrower can sustain the required monthly payment. The mistake most homeowners make is treating the promotional period as a 0% term loan and making minimum payments, only to discover a retroactive interest charge when the period ends.

Conclusion

Roof financing in 2026 is more accessible than most homeowners realize. Home equity loans and HELOCs remain the lowest-rate path for homeowners with established equity, with national averages in the 7.23-7.87% range as of March 2026. Contractor point-of-sale financing through platforms like GreenSky delivers genuine 0% short-term financing for borrowers who can sustain aggressive payoff schedules. FHA Title I fills the gap for homeowners with limited equity and solid income. Personal loans remain the option of last resort, best reserved for emergency situations where speed of funding outweighs the cost of higher interest rates.

If insurance is on the table, exhaust that path first. Over James Carver's 20-year career spanning 1,800+ residential projects across the U.S. South and Midwest, insurance coverage — where applicable — remains the single largest reducer of out-of-pocket roofing costs.

Whatever path you choose, do not delay. A roof that needs replacement this month costs $13,000 now. A roof that needed replacement last year and was deferred costs $13,000 plus the interior damage that accumulated in the interim.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Loan rates, terms, and eligibility requirements change frequently and vary by lender, credit profile, and geographic market. Consult a qualified financial advisor, tax professional, or HUD-approved housing counselor before making any borrowing decision. Interest deductibility claims are subject to IRS rules and your individual tax situation.

Sources & References

[1] National Roofing Contractors Association (NRCA) — Roofing Cost Benchmarks

[2] Bankrate — Current Home Equity Loan Rates, March 2026

[3] Bankrate — Current HELOC Rates, March 2026

[4] GreenSky — Home Improvement Financing Program

[5] Bankrate — Best Personal Loan Rates, March 2026

[6] HUD.gov — FHA Title I Property Improvement Loan Program

James is a licensed roofing contractor with 20 years of experience in roof installation, inspection, and repair across the U.S. South and Midwest. He specialises in asphalt shingles, metal roofing, and storm damage restoration. On NearbyHunt, James offers practical advice on roof maintenance, insurance claims, and selecting the right materials for long-lasting protection.

Jacob is a licensed roofing contractor with over 18 years of experience in roof inspection, installation, and restoration. Based in Texas, he has led hundreds of successful roofing projects across residential and commercial properties. Jacob is also a certified storm damage specialist, ensuring that all NearbyHunt roofing content meets industry best practices and safety standards.